Can You Trust Your Trust?

Trusts in Portugal: smart planning if structured right, costly if you get control wrong.

Trusts are a familiar and widely used tool in common-law jurisdictions. They are often associated with estate planning, asset protection, or family governance. But once a Portuguese tax resident enters the picture, the question becomes unavoidable:

Can you trust your trust — from a Portuguese tax perspective?

The short answer is: sometimes, but only if you understand how Portugal looks through trusts, when it taxes them, and who it considers taxable at each stage.

This article explains, in plain terms, how trusts are taxed in Portugal today, including:

- why Portugal does not “recognise” trusts in civil law but still taxes them;

- when income can be taxed under CFC (Controlled Foreign Corporation) rules;

- how distributions and liquidations are treated; and

- where the real risks usually lie.

1. Trusts in Portugal: Not Recognised, Yet Taxed

Portugal is a civil-law jurisdiction and does notrecognise trusts as a domestic legal institution. There is no Portuguese “TrustLaw”, and trusts cannot be created under Portuguese civil law.

However, this does not mean trusts are ignored fortax purposes.

Since the 2014 IRS reform, Portuguese tax law explicitly refers to “estruturas fiduciárias” (fiduciary structures), a deliberately broad concept designed to capture:

- discretionary trusts;

- irrevocable and revocable trusts;

- foreign family trusts; and

- similar arrangements governed by foreign law.

In other words, Portugal taxes the economic reality,not the civil-law label.

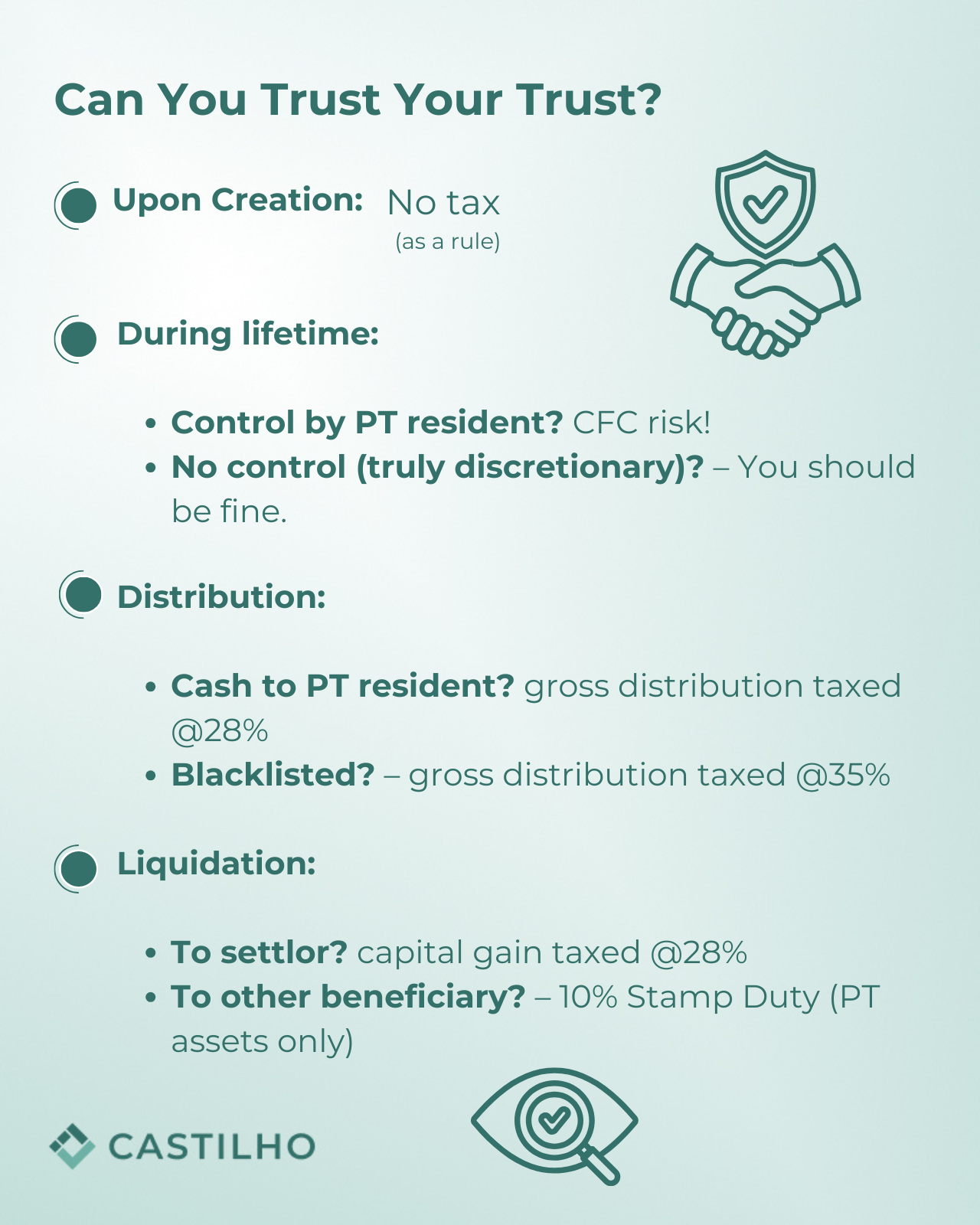

2. No Tax on Creation — But This Is Not a Free Pass

As a general rule, Portugal does not tax the creation ofa trust.

The transfer of assets by a settlor to a foreign trust is not,by itself, treated as:

- a taxable disposal for capital gains purposes; nor

- a taxable donation subject to Stamp Duty.

This position is consistent with Portuguese administrative doctrine and reflected in binding rulings, including where significant assets were transferred to discretionary trusts governed by Jersey law.

That said, this “no tax at inception” approach should not be confused with long-term tax neutrality. The real tax exposure usually arises later, during the life of the trust.

3. The Big Risk: CFC Rules Applied to Trusts

3.1 What Are CFC Rules?

These rules allow Portugal to tax undistributed profits of foreign entities if:

- they are located in a low-tax jurisdiction, and

- they are controlled by Portuguese tax residents.

Crucially, the law explicitly extends this concept of control to situations involving:

“mandatário,fiduciário ou interposta pessoa”

(agent, fiduciary, or interposed person)

This wording is what brings trusts into the CFC net.

3.2 Can a Trust Trigger CFC Taxation?

Yes — but not automatically.

Portuguese tax authorities have clarified that a trust only triggers CFC taxation if the Portuguese resident effectively controls it.

In a landmark binding ruling involving a Jersey discretionary trust, the AT accepted that no CFC imputation applied where:

- the settlor had no legal or factual control over assets;

- the trustee had full discretion over income and capital;

- beneficiaries resident in Portugal were explicitly excluded while resident; and

- no one resident in Portugal held enforceable rights over the trust’s income or assets

This ruling is critical: discretion matters.

3.3 When CFC Risk Becomes Real

CFC exposure becomes significant where:

- the settlor retains powers (revocation, veto, appointment);

- the beneficiary has fixed or enforceable rights;

- the trust is effectively “transparent” or nominee-like; or

- the structure is located in a blacklisted or low-tax jurisdiction and lacks economic substance.

In these cases, Portugal may attribute undistributed income annually to the Portuguese resident, taxed at progressive IRS rates.

4. Taxation of Distributions: When Money Actually Flows

When a trust makes distributions of income (notliquidation), Portugal taxes the recipient if they are resident.

Since 2014, amounts distributed by fiduciary structures are classified as:

- Category E – investment income, and

- taxed at a 28% flat rate (or 35% if the trust is in a blacklisted jurisdiction).

Importantly:

- distributions are only taxed if they were not already taxed under CFC rules;

- this avoids double taxation of the same income.

This change closed a major gap that previously existed under Portuguese law.

5. Liquidation of a Trust: Where Stamp Duty May Appear

The most sensitive moment is often liquidation or extinction of the trust.

Portuguese law distinguishes two scenarios:

5.1 Liquidation in Favour of the Settlor

If the settlor receives assets back:

- the difference between what was contributed and what is received may be taxed as a capital gain, and

- taxed at a 28% rate, subject to adjustments for prior CFC taxation.

This mirrors the tax treatment of company liquidations.

5.2 Liquidation in Favour of a Beneficiary (Not the Settlor)

Here, Portugal treats the transfer as a gratuitous acquisition.

As a rule:

- Stamp Duty at 10% applies,

- only if the assets are deemed located in Portugal.

If the trust assets consist solely of:

- foreign shares,

- foreign securities, or

- non-Portuguese bank accounts,

then Stamp Duty does not apply, due to lack of territorial connection — a position expressly confirmed by the AT in binding rulings

6. What This Means in Practice

From a Portuguese tax perspective, a trust is not inherently aggressive or abusive.

But it is also never neutral by default.

Everything depends on:

- control;

- discretion;

- residence of parties;

- timing of distributions; and

- location of underlying assets.

The same trust can be:

- perfectly acceptable in one configuration, and

- fully taxable in another.

7. Final Thoughts: Can You Trust Your Trust?

You can — if it is properly structured and understood.

Portugal does not prohibit trusts, nor does it automaticallypenalise them. But it will:

- look through form to substance;

- impute income where control exists; and

- tax distributions and liquidations with precision.

For Portuguese residents, the real risks are rarely at the start — they arise over time, often unintentionally.

If a trust was created abroad, do not assume it is invisible to Portuguese tax law. It almost never is.